In this article

- 1. What Is Estimated Chargeable Income (ECI)?

- 2. Why Does IRAS Require ECI Filing?

- 3. Who Needs to File ECI in Singapore?

- 4. Can a Company Qualify for an ECI Filing Waiver?

- 5. What Does Nil ECI Actually Mean?

- 6. Which Entities Are Not Required to File ECI?

- 7. How Is ECI Different From Form C-S?

- 8. When Must Companies File ECI?

- 9. Why Does Filing ECI Early Matter?

- 10. How To Calculate Estimated Chargeable Income (ECI)?

- 11. What Are Common ECI Filing Mistakes?

- 12. What Happens If ECI Is Filed Late?

- 13. Estimated Chargeable Income (ECI) FAQs

For many business owners in Singapore, tax season feels like something that is to be taken care of only once a year. The reality is a little different, because long before a company submits its corporate income tax return, IRAS expects it to provide an estimate of its taxable income. This requirement is known as Estimated Chargeable Income (ECI), and it catches many companies off guard than you might think.

It is particularly common among startups and smaller businesses. Founders spend months focused on customers, hiring, product development, and revenue targets. Tax compliance often gets pushed down the priority list until a reminder arrives from IRAS.

By then, the filing deadline may be much closer than expected. While ECI filing is a regulatory requirement, viewing it solely through a compliance lens misses the bigger picture. When done properly, it can help businesses understand their financial position earlier, prepare for tax obligations, and make better cash flow decisions.

What Is Estimated Chargeable Income (ECI)?

Ask a first-time founder what ECI means and chances are they’ll confuse it with the annual corporate tax return. That misunderstanding is surprisingly common.

Estimated Chargeable Income (ECI) is essentially a company’s estimate of its taxable profits for a particular Year of Assessment (YA). It is calculated after deducting tax-allowable business expenses but before applying certain tax exemptions available under Singapore’s corporate tax system.

At the point when ECI is filed, many companies might not have completed their audited financial statements yet. Instead, they use available financial information, management accounts, and internal records to arrive at a reasonable estimate for just reporting a rough figure to IRAS.

Think of ECI as an early forecast rather than a final declaration. The actual tax position may change later when the company files Form C-S or Form C.

Read also: IRAS Employer Tax Filing Deadline 2026: Submit by 1 March

Why Does IRAS Require ECI Filing?

From a business owner’s perspective, it can feel like an extra formality.

Why estimate taxes now if a full tax return will be submitted later?

IRAS uses ECI filings to obtain an early indication of corporate earnings across the economy. This allows tax authorities to assess expected tax revenue and manage tax administration more effectively.

There is also a practical advantage for companies. When businesses estimate their taxable income early, they are forced to take a closer look at their financial performance. In many cases, ECI preparation reveals issues that might otherwise remain hidden until much later.

A company may discover that expenses are rising faster than revenue. A profitable year may be generating a larger tax bill than expected. Or a startup may realise its losses are greater than initially projected. These insights are often useful long before the annual tax filing deadline arrives.

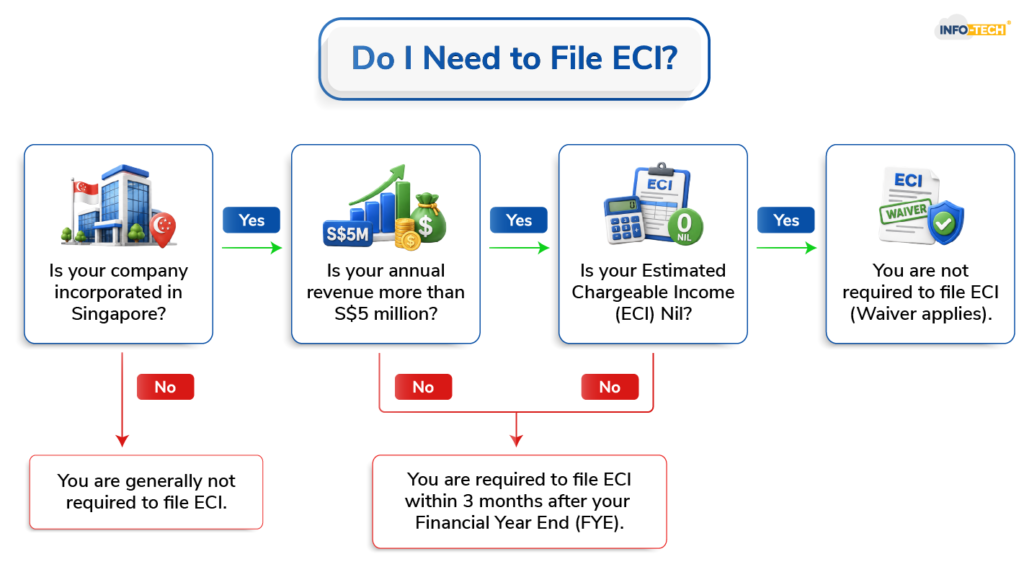

Who Needs to File ECI in Singapore?

One of the biggest myths surrounding ECI is that it only applies to large companies. In reality, that is not how it actually works. Most Singapore-incorporated companies are required to file ECI within three months from the end of their financial year.

That includes:

- SMEs

- Startups

- Private limited companies

- Family-owned businesses

- Professional service firms

- Technology companies

Whether the business employs three people or three hundred, the filing obligation generally remains the same unless a waiver applies.

This is where some younger companies run into trouble. They assume low revenue means no filing requirement. They assume no profits means no filing requirement. Neither assumption is always correct.

Read also: Income Tax Filing Guidelines for Singapore Businesses

Can a Company Qualify for an ECI Filing Waiver?

Yes, but the waiver conditions are often standard. To qualify for an ECI filing waiver, a company must satisfy both conditions:

| Requirement | Condition |

|---|---|

| Annual Revenue | S$5 million or below |

| ECI | Nil |

A company with S$4 million in revenue and nil ECI may qualify for the waiver. But a company with S$4 million in revenue and S$20,000 ECI will still need to file.

Likewise, a company with S$10 million in revenue and nil ECI may also need to file because it exceeds the revenue threshold.

Many business owners focus only on profitability and overlook the revenue requirement. That’s where mistakes happen.

What Does Nil ECI Actually Mean?

The term “nil ECI” sounds straightforward. In practice, it often isn’t. Some companies assume it simply means having no profit. Others assume it means generating no revenue. Neither interpretation is entirely accurate.

Nil ECI means the company’s estimated chargeable income is zero before deducting exemptions under schemes such as startup tax exemptions or partial tax exemptions. A company can still generate revenue and even report accounting profits while arriving at a nil ECI position after tax adjustments are made.

This is why finance teams generally review tax computations carefully rather than relying on accounting profit alone.

Which Entities Are Not Required to File ECI?

Apart from companies qualifying for the filing waiver, certain entities are generally exempt from ECI filing obligations. These include:

- Foreign universities

- Certain foreign ship owners and charterers

- Approved CPF unit trusts

- Designated unit trusts

- Certain real estate investment trusts

- Entities granted specific exemptions by IRAS

For the average SME, however, these exemptions rarely come into play. Most private companies should assume ECI filing applies unless there is a clear reason otherwise.

Read also: IR8A, IR8S and IR21 – How to File with Ease This Tax Season

How Is ECI Different From Form C-S?

A surprising number of business owners think ECI and Form C-S are the same thing. They are not. One is an estimate. The other is the final declaration.

| Feature | ECI | Form C-S / Form C |

|---|---|---|

| Purpose | Estimate taxable income | Final corporate tax return |

| Timing | Within 3 months after FYE | Annual tax filing season |

| Figures Used | Estimated figures | Final figures |

| Assessment Stage | Preliminary | Final |

| Instalment Benefits | Available | Not applicable |

An easy way to think about it is this: ECI tells IRAS what you expect your tax position to be. Form C-S confirms what it actually turned out to be.

When Must Companies File ECI?

The filing deadline is one of the most important dates to remember. Companies generally have three months from the end of their financial year to submit ECI.

For example:

| Financial Year End | ECI Filing Deadline |

|---|---|

| 31 December | 31 March |

| 31 March | 30 June |

| 30 June | 30 September |

| 30 September | 31 December |

Why Does Filing ECI Early Matter?

Most businesses focus on filing before the deadline. Fewer think about filing earlier than required. Yet filing early can provide a significant cash flow advantage.

IRAS offers instalment payment arrangements for qualifying companies that submit their ECI promptly and maintain GIRO arrangements.

| Filing Timing | Instalments Available |

|---|---|

| Within 1 month of FYE | Up to 10 |

| Within 2 months of FYE | Up to 8 |

| Within 3 months of FYE | Up to 6 |

| After 3 months | None |

For a growing SME, spreading tax payments across multiple months can be far easier than making a single lump-sum payment. Cash flow is often the difference between a manageable tax bill and a stressful one.

How To Calculate Estimated Chargeable Income (ECI)?

Many expenses recorded in financial statements are not automatically deductible for tax purposes. Likewise, some tax deductions do not appear directly in accounting records. The process generally starts with accounting profit and then adjusts for tax treatment.

What Expenses Are Commonly Added Back?

Some expenses are not tax-deductible and therefore need to be added back. Like:

- Certain fines and penalties

- Private expenses

- Depreciation

- Private vehicle expenses

What Expenses Are Commonly Deductible?

- Employee salaries

- CPF contributions

- Office rent

- Utilities

- Professional fees

- Business-related operating costs

What Expenses Are Deductible and Non-Deductible?

| Generally Deductible | Generally Non-Deductible |

|---|---|

| Salaries | Traffic fines |

| CPF Contributions | Private expenses |

| Office Rent | Personal entertainment |

| Utilities | Private vehicle costs |

| Professional Fees | Capital expenditure |

Which Information Should Be Prepared Before Filing ECI?

Companies typically gather:

- Management accounts

- Revenue records

- Expense schedules

- Capital allowance information

- Company UEN

- Corppass authorisation

- Supporting financial reports

Businesses that maintain organised records throughout the year usually find ECI filing far less stressful than those businesses that prepare for it last minute. Those relying on spreadsheets scattered across multiple departments often face a much harder process.

How Do Companies File ECI?

First, the authorised individual must have the appropriate Corppass permissions.

The company then accesses the IRAS myTax Portal, enters the required financial information, reviews the submission, and files electronically.

The technical steps are simple. The accuracy of the numbers is where most of the real work happens.

Read also: How Much Is GST in Singapore (2026)?

What Are Common ECI Filing Mistakes?

Companies often:

- Assume they qualify for a waiver without checking

- Confuse accounting profit with taxable income

- Miss the filing deadline

- Use incomplete financial data

- Forget tax adjustments

- Underestimate revenue

The mistakes themselves are usually not complicated, but the consequences can be.

What Happens If ECI Is Filed Late?

When ECI is not filed on time, IRAS may issue an Estimated Notice of Assessment (NOA). This assessment is based on information available to the tax authority, including previous filings and historical records. The challenge is that the estimate may not reflect the company’s actual financial performance.

Once issued, businesses generally need to address the assessment while simultaneously resolving the filing issue. They may also lose eligibility for instalment payment arrangements.

This is a situation most finance teams would rather avoid.

How Should Startups Approach ECI Filing?

Startups often operate differently from established businesses. Resources are limited. Finance teams are small. Processes are still evolving. This makes it even more important to establish good habits early.

Founders who maintain proper bookkeeping, payroll records, employee expense tracking, and financial reporting from day one generally face fewer compliance challenges as the company grows.

The startups that struggle with ECI are rarely the ones with complex tax situations. More often, they simply lack organized records.

Read also: Withholding Tax Singapore: A Guide For Businesses

Conclusion

For many businesses, Estimated Chargeable Income (ECI) starts out as another compliance deadline on the calendar. Over time, most realize it serves a bigger purpose.

Preparing ECI encourages companies to understand their numbers earlier, anticipate tax obligations, and improve financial discipline. It also highlights how interconnected different business functions really are. Payroll records affect expense calculations. Employee benefits influence deductions. Financial reporting shapes tax estimates.

When those records are scattered across multiple systems, preparing accurate filings becomes far more difficult than it needs to be. This is one reason many growing companies adopt integrated HRMS and payroll software. Having employee data, payroll information, leave records, claims, and reporting tools in one place helps finance and HR teams work from the same source of truth. The result is not just smoother payroll processing, but stronger compliance and better visibility when tax filing season arrives.

Ultimately, ECI is not just about meeting a deadline. It is about building the financial habits that help a business stay organised, compliant, and prepared for growth.

Read also: Ways to Reduce Income Tax for Singapore Tax Residents

Estimated Chargeable Income (ECI) FAQs

What is ECI estimated chargeable income?

Estimated Chargeable Income (ECI) is an estimate of a company’s taxable profits for a Year of Assessment, submitted to IRAS before the final corporate tax return is filed.

How to calculate Singapore ECI?

ECI = Profit Before Tax + Non-Deductible Expenses − Capital Allowances − Tax Deductions In simple terms, take your company’s profit, add back expenses that IRAS doesn’t allow, subtract eligible tax deductions, and the result is your Estimated Chargeable Income (ECI).

When not to file ECI?

A company does not need to file ECI if its annual revenue is S$5 million or below and its ECI is nil, or if it belongs to specific exempt entities recognised by IRAS.

How to reduce chargeable income in Singapore?

Companies can reduce chargeable income legally by claiming tax-deductible business expenses, capital allowances, approved donations, and available tax reliefs, which lower their taxable profits before corporate tax is calculated., all data can be accessed at anytime, anywhere.