| The Central Provident Fund (CPF) is Singapore’s mandatory social security savings scheme. Both employees and employers contribute to three main accounts: Ordinary Account (OA), Special Account (SA), and MediSave Account (MA). CPF savings can be used for housing, healthcare, retirement income, and approved investments. Contribution rates vary by age and wages. |

What Is CPF and Why It Matters in Singapore

The Central Provident Fund (CPF) is Singapore’s compulsory savings scheme for working Singapore Citizens and Permanent Residents. Established to support retirement adequacy, CPF today plays a much broader role, helping Singaporeans fund housing, healthcare, insurance, and retirement income.

CPF is not just a retirement fund. It is a structured government-backed system that:

- Ensures long-term retirement savings

- Helps members afford HDB or private housing

- Covers hospitalisation and approved medical expenses

- Provides lifelong monthly payouts through CPF LIFE

- Encourages disciplined savings through mandatory contributions

Unlike voluntary savings accounts CPF contributions are deducted from wages and matched by employers.

How CPF Contributions Work in Singapore

CPF contributions are mandatory for employees earning more than $50 per month. Both the employer and employee contribute a percentage of the employee’s monthly wages.

Contribution rates depend on:

- Age group

- Wage amount

- Citizenship status

- Type of wages (Ordinary Wages vs Additional Wages)

| If you would like a deeper breakdown of contribution formulas, wage ceilings, and employer obligations, read our complete guide on CPF Contribution in Singapore |

Current CPF Contribution Rates (Below 55 Years Old)

| Contributor | Contribution Rate | Allocation Basis |

| Employer | 17% | Of employee’s monthly wages |

| Employee | 20% | Deducted from salary |

| Total | 37% | Credited to CPF accounts |

For older employees, contribution rates see a progressive reduction to support employability while retirement savings growth continues.

CPF Allocation Rates by Age (Below 55 Example)

For members aged 35 and below:

| Account | Allocation % (of Total CPF Contribution) |

| Ordinary Account (OA) | 23% |

| Special Account (SA) | 6% |

| MediSave Account (MA) | 8% |

As members age, a higher portion goes to Special Account and MediSave to strengthen retirement and healthcare savings.

Where Do My CPF Contributions Go?

Your monthly CPF contributions get distributed into three main accounts:

1. Ordinary Account (OA)

The OA serves these primary purposes:

- Buying HDB flats or private property

- Paying housing loans

- Approved CPF investments

- Education under CPF Education Scheme

- Insurance premiums (e.g., Home Protection Scheme)

Interest Rate: Minimum 2.5% per annum (extra interest for first $60,000 combined balances).

2. Special Account (SA)

The SA is for retirement-related purposes and long-term investment.

You can use it for:

- Retirement savings

- CPF Retirement Sum formation

- Approved low-risk CPF investment products

Interest Rate: Minimum 4% per annum (higher than OA to encourage long-term compounding).

3. MediSave Account (MA)

MediSave is dedicated to healthcare expenses.

It can be used for:

- Hospitalisation bills

- Day surgeries

- Approved outpatient treatments

- MediShield Life premiums

- CareShield Life premiums

- ElderShield supplements

Interest Rate: Minimum 4% per annum.

Because CPF contribution rates vary by age and are subject to wage ceilings, using a CPF calculator is highly recommended. It allows both employees and HR teams to simulate contribution breakdowns across Ordinary, Special, and MediSave Accounts before finalising payroll figures.

What Can Your Central Provident Fund Be Used For?

CPF is a multi-purpose financial pillar in Singapore. Below is a structured overview for clarity.

CPF Usage Summary Table

| Purpose | Account Used | Key Conditions |

| Buy HDB Flat | OA | Subject to Valuation Limit |

| Pay Housing Loan | OA | For HDB or approved private property |

| Hospital Bills | MA | Subject to withdrawal limits |

| Insurance Premiums | MA / OA | Approved schemes only |

| Education | OA | For approved local institutions |

| Retirement Income | RA (formed at 55) | CPF LIFE payouts from 65 |

| Investments | OA / SA | Under CPF Investment Scheme |

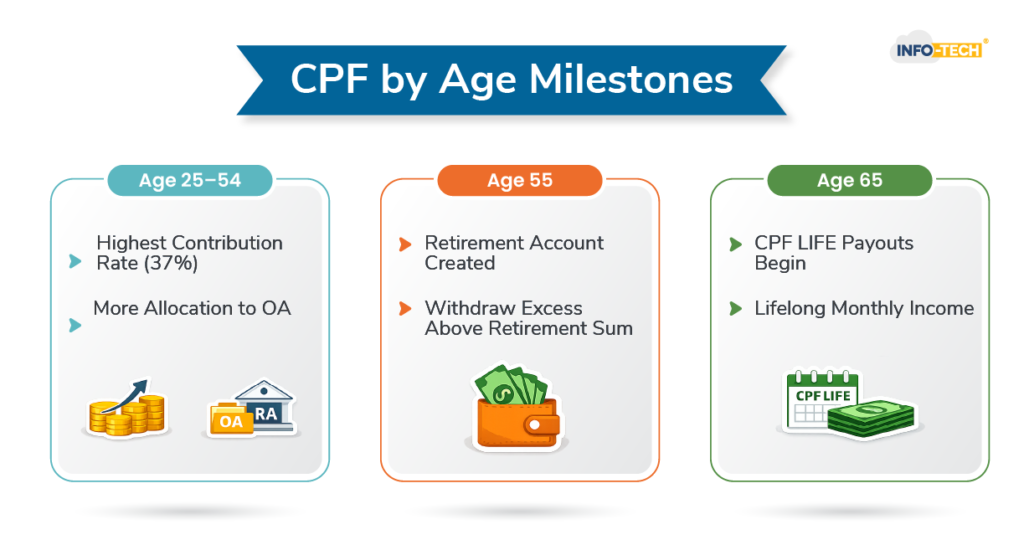

How CPF Supports Retirement: What Happens at 55 and 65

At age 55, CPF members will have a Retirement Account (RA) created. The system transfers funds from the SA and OA into the RA up to the Full Retirement Sum (FRS).

Singapore structures Retirement Sums as:

- Basic Retirement Sum (BRS)

- Full Retirement Sum (FRS)

- Enhanced Retirement Sum (ERS)

These sums have a direct impact on monthly CPF LIFE payouts starting from age 65.

CPF LIFE gives you lifelong monthly income protecting you against longevity risk.

How to Turn CPF Into Cash

CPF serves for long-term security, but there are ways to withdraw funds under regulated conditions.

You can withdraw CPF:

- At age 55 (excess above required retirement sum)

- At age 65 (monthly CPF LIFE payouts begin)

- If you leave Singapore

- Under medical grounds

- For specific housing refunds

Keep in mind:

CPF is not withdrawable like a bank savings account. Withdrawals are structured so that there is adequacy for retirement.

| To avoid costly retirement planning mistakes, explore our detailed guide on 5 CPF Withdrawal Mistakes to Avoid. |

Interest Rates and Extra Interest Benefits

CPF offers attractive risk-free interest rates:

- OA: 2.5% minimum

- SA & MA: 4% minimum

- Extra 1% interest on first $60,000 of combined balances

- Additional extra 1% on first $30,000 for members aged 55 and above

This structure gives a boost to retirement compounding over time.

Why CPF Is Considered a Strong Social Security System

CPF works because it integrates:

- Mandatory contributions

- Government-guaranteed interest

- Healthcare financing

- Housing affordability support

- Lifetime retirement payouts

This creates a reduction in dependency on welfare systems while encouraging personal responsibility and disciplined savings.

Final Thoughts:

CPF remains one of the strongest structured savings systems, combining forced savings discipline with government-backed security and lifetime income support.

More than just a payroll deduction — it is Singapore’s integrated social security system covering housing, healthcare, retirement, and insurance protection.

Understanding how contributions are allocated, how interest compounds, and what CPF savings can be used for allows individuals to make better financial and retirement decisions.

This is why many Singapore companies today rely on integrated HRMS and Payroll software with automated CPF computation modules to ensure accuracy and compliance.

Central Provident Fund Frequently Asked Questions

What can your CPF be used for?

CPF can be used for housing (HDB or private property), healthcare expenses approved insurance premiums tertiary education, retirement income and approved investments. Funds are allocated into different CPF accounts — OA, SA and MA — each designed for specific purposes to ensure long-term financial security and retirement adequacy.

How does CPF contribution work in Singapore?

CPF contributions are mandatory for eligible employees and employers. Employees contribute up to 20% of monthly wages, while employers contribute up to 17%, depending on age. The total contribution is split into Ordinary, Special, and MediSave Accounts. Contribution rates decrease after age 55.

Where do my CPF contributions go?

Your CPF contributions are distributed into three accounts: Ordinary Account (for housing and investments), Special Account (for retirement savings), and MediSave Account (for healthcare expenses). At age 55, savings from OA and SA are transferred to a Retirement Account to fund CPF LIFE payouts.

How to turn CPF into cash?

CPF can be withdrawn at age 55 (amounts above retirement sum), and monthly payouts begin at age 65 under CPF LIFE. Early withdrawals are allowed under specific circumstances such as permanent departure from Singapore or medical grounds. CPF has been designed to provide long-term retirement and healthcare security.