IRAS Employer Tax Filing Deadline 2026

The IRAS employer tax filing deadline for 2026 is 1 March 2026. By this date, employers must submit employee income information for income paid between 1 January and 31 December 2025. This submission allows IRAS to assess employees’ personal income tax accurately under Year of Assessment (YA) 2026.

Employer tax filing is a statutory reporting obligation, not a tax payment. Even if a company is loss-making, dormant for part of the year, or has only one employee, filing is required if employment income was paid.

| Deadline: 1 March 2026 Applies to: All employers who paid employment income in 2025 |

What Is Employer Tax Filing in Singapore?

Employer tax filing refers to the annual reporting of employee remuneration to IRAS under the Income Tax Act.

The information submitted forms the basis of employees’ individual income tax assessments. Employers are not paying tax during this process; they are reporting income details.

This requirement is separate from:

– Corporate income tax filing

– CPF submissions

– GST reporting

Employers act as income reporters and must ensure that the data submitted is accurate and complete.

Who Must File for YA 2026?

Any employer who paid employment income in Singapore during 2025 must submit income information to IRAS by 1 March 2026. There is no exemption based on company size or headcount.

This includes:

- Companies with only one employee

- Employers paying directors’ fees

- Businesses engaging part-time or contract staff

- Employers with foreign employees

If income was paid, filing is mandatory even if the employee has since resigned or worked only briefly during the year.

| Any employer who paid employment income in Singapore during 2025 must submit employer tax information to IRAS by 1 March 2026. |

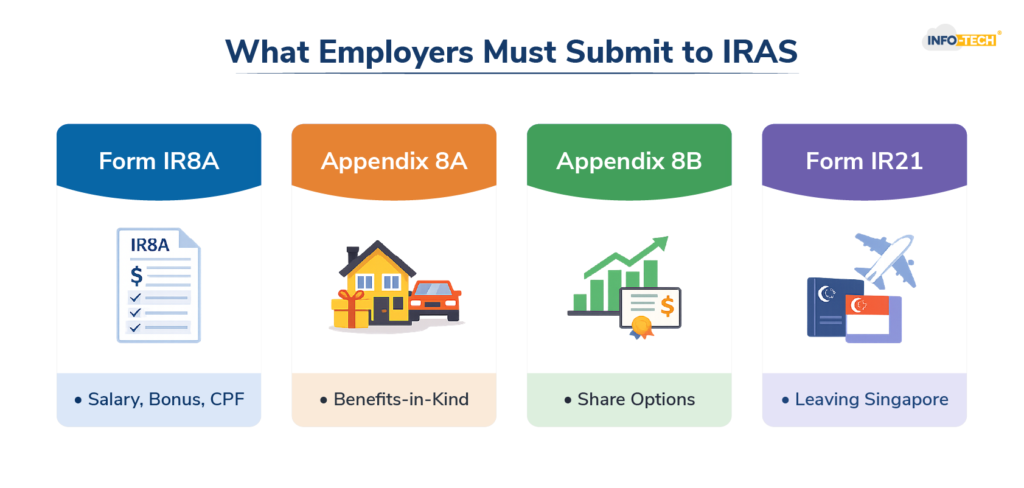

What Must Employers Submit to IRAS?

The primary document required is Form IR8A, which reports each employee’s total remuneration for the year. This includes salary, bonuses, allowances, CPF contributions, and director’s fees.

Depending on the employee’s compensation structure, employers may also need to submit additional supporting forms:

- Appendix 8A for benefits-in-kind such as company cars or housing

- Appendix 8B for employee share options or share awards

- Form IR21 for employees who ceased employment or left Singapore

Employers must ensure that all forms submitted are consistent with payroll and CPF records.

Auto-Inclusion Scheme (AIS) for YA 2026

The Auto-Inclusion Scheme (AIS) allows employers to transmit employee income data electronically to IRAS instead of issuing IR8A forms to employees. Employers under AIS submit income information directly through IRAS-approved systems.

Employers who had 5 or more employees in the preceding year are required to participate in AIS. IRAS may also notify certain employers to join AIS even if headcount is lower.

| Employers on AIS do not issue IR8A forms to employees — IRAS receives the data directly. |

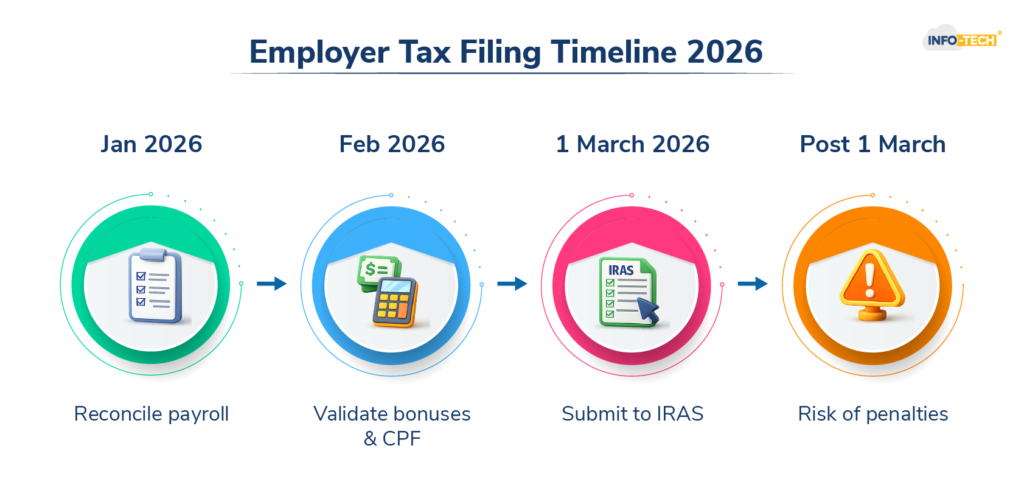

Employer Tax Filing Timeline for YA 2026

Employer tax filing follows a fixed annual cycle. Income earned between 1 January and 31 December 2025 must be consolidated, reviewed, and submitted by 1 March 2026.

Most compliance issues arise when employers delay data reconciliation until February. Late preparation increases the risk of missing bonuses, benefits-in-kind, or CPF adjustments that should be reported to IRAS.

Consequences of Late or Incorrect Employer Filing

IRAS considers employer income reporting a legal obligation. Late submissions or inaccurate filings may result in enforcement actions under the Income Tax Act.

Possible consequences include:

- Monetary penalties

- Estimated income assessments issued by IRAS

- Follow-up compliance reviews or audits

- Loss of employee confidence due to incorrect tax bills

| Repeated non-compliance may trigger IRAS to review payroll reporting practices more closely. |

Common Employer Mistakes That Lead to Non-Compliance

Many filing issues stem from operational gaps rather than intent. Employers frequently encounter problems due to inconsistent payroll records, manual calculations, or miscommunication between HR and finance teams.

Other common issues include failing to declare non-cash benefits, overlooking variable pay, or submitting outdated employee information. These errors become more likely as organisations grow or adopt flexible and hybrid work arrangements.

How Employers Can Prepare Effectively for the 1 March 2026

The most reliable way to meet the IRAS deadline is to treat employer tax filing as a year-round payroll discipline, not a once-a-year task. Regular reconciliation of payroll, CPF, bonuses, and leave encashment helps ensure that year-end reporting is accurate and complete.

Many employers now rely on integrated payroll and leave management software to centralise employee data, reduce manual errors, and maintain audit-ready records throughout the year. This approach significantly reduces last-minute compliance risks.

Final Takeaway

The IRAS employer tax filing deadline for YA 2026 is 1 March 2026.

If your organisation paid employment income in 2025, submission is required regardless of company size or profitability.

Timely and accurate reporting protects both the organisation and its employees from unnecessary penalties, corrections, and administrative issues.

Early preparation is the safest compliance strategy.

Frequently Asked Question

What is the IRAS employer tax filing deadline for 2026?

The deadline is 1 March 2026 for income earned in 2025.

Do small companies need to submit IR8A?

Yes. Employers with even one employee must file unless exempted under AIS rules.

Is employer tax filing the same as corporate tax filing?

No. Employer tax filing reports employee income, while corporate tax filing reports company profits.

Do employers pay tax when submitting IR8A?

No. Employers only report income; employees pay the personal income tax assessed by IRAS.